English

English Español

Español Français

Français Deutsch

Deutsch Italiano

Italiano Português

Português

Let’s review the climate investment goals of the Paris Agreement and compare them to our global wealth. Individually, we can make a profit and improve the climate by investing in Green Bonds.

Climate investment goals

According to the latest report from the Independent High-Level Expert Group on Climate Finance (Bhattacharya et al., 2024), the projected investment requirements to meet the goals of the Paris Agreement are:

These requirements include the different investment needs:

Alternative energy production and energy efficiency (clean energy transition).

Adaptation and resilience.

Loss and damage.

Increasing natural capital.

And a just transition.

The amounts for the different needs are given the table below.

Clean energy transition dominates, followed by adaptation and resilience and loss and damage, which reach 40 percent of the total in EMDCs other than China.

Also notable is our low level of investment in the latest year, 2022. For EMDCs, the annual investments should increase five-fold, indicating the challenge. The request for climate investments also competes with needs for nutrition, health care, and economic development.

“A big push is required on three priorities: (i) to prepare and implement high-quality investments; (ii) to put in place the necessary macroeconomic and sectoral policy and institutional reforms and tackle the severe constraints facing many countries due to high debt and limited fiscal space; and (iii) to mobilize finance at scale and improve access to affordable capital" (Bhattacharya et al., p.7, 2024).

Of course, these investments provide long-term benefits in terms of infrastructure, electricity supply, energy savings, adaptation protection, job creation, and a just transition.

The annual potential savings in the year 2030 are estimated. At the upper range, the total benefits are USD 36 trillion per year, about five times the annual investment goal of USD 6.7 trillion per year (Bhattacharya et al., p.21, 2024).

The benefits are multiple, including:

Reduced fossil fuel investments in exploration and production.

Reduced fuel costs from fossil fuel consumption.

Reduced energy costs of renewables and efficiency.

Reduced operation and maintenance costs.

Phase-out of fossil fuel and environmentally harmful subsidies.

Reduced input costs from pesticides and fertilizers.

Reduced economic costs due to productivity increases, fewer damages to assets, and disruptions in economic activity.

Reduced environmental and social costs, including better health and well-being, increased biodiversity, less conflict and migration, fewer global and local inequities.

Growth and development benefits, such as job creation, the use of more efficient technologies, improved ecosystem services, and enhanced viability through risk reduction.

Social benefits of strengthened social stability and overall societal well-being.

The climate objectives and benefits are compared to global household wealth to give a perspective.

Global household wealth in 2020

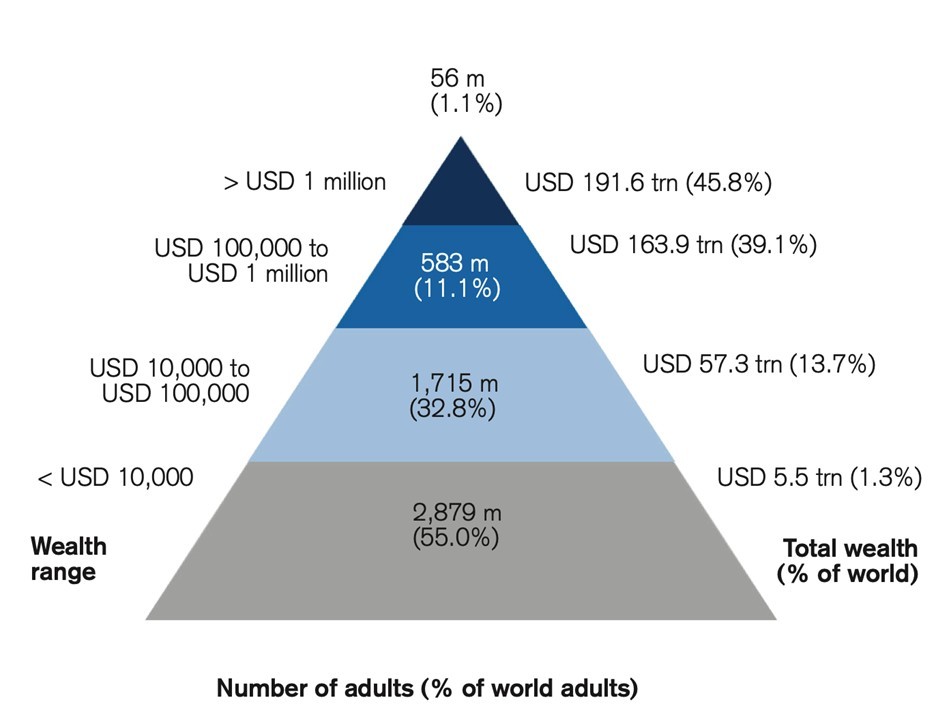

Credit Suisse has reported on global household wealth for years, their last detailed research covers 2020 and is pictured below (Shorrocks et al.,2021).

Four wealth ranges are shown: at the top, those having more than USD 1 million wealth, a second range from USD 100,000 to 1 million, a third range from USD 10,000 to 100,000, and the lowest range less than USD 10,000. On the right side is shown the total wealth held by the adults in the given wealth ranges. One sees that $191.6 trillion in wealth is held by the top group, which represents 45.8% of the total wealth of the world. The second group owns 163.9 trillion dollars, which represents 39.1% of the total wealth, and so on. In the middle of the pyramid is indicated the number of adults (and % of world adults) for each group.

It is noteworthy that the wealth of the first two categories of rich adults, with more than USD 1 million and with USD 100,000 to USD 1 million, totals USD 336 trillion. Thus, the overall climate objective expenditure of USD 6.7 trillion in 2030 is 2.0 percent of the combined wealth of the top two classes of wealthier individuals.

The growth in wealth is also interesting: for the following three years, 2021 to 2023, for which we have data, the average annual growth in wealth is 3.4 percent. This is in contrast to the average annual growth of 6 percent per year in the preceding decade. Annual growth in wealth will likely continue to be greater than the climate investment goal of the Paris Agreement to restore our climate. Do the wealthier individuals know the magnitude of their wealth compared to the need for investments to save our planet’s climate? The global answer is 50 to 1. These investments can be thought of as an insurance policy. Also, others, governments, corporations, international banks will be making substantial climate investments.

Green bonds are a straightforward form of investment in climate improvement. You obtain a positive financial return while helping to improve the planet’s climate.

Green bonds

These are fixed-income instruments (bonds) that fund environmental projects. Although they represent only a small percentage of the global bond market, their size is expected to exceed $2 trillion this year.

The projects usually involve alternative energy production and/or energy efficiency. However, they may also involve adaptation and resilience, loss and damage, increasing natural capital, and a just transition. Large green bond offerings usually combine various types of ecological projects. The projects to be realized are described in the bond prospectus, which the investor should read carefully. The bond interest and principal are to be repaid to the investor independently of the degree of completion of the projects.

The issuers of green bonds also can vary widely from municipalities involved in building local wind turbines, to large companies like Apple, which issued a green bond to realize renewable energy and energy savings projects within its factories, to government bonds for environmental purposes.

In the US, green bonds often exempt the shareholder from gross income for federal income tax purposes. They align with the guidelines outlined in ICMA's Green Bond Principles and may meet the more rigid standards developed by the Climate Bond Imitative, which require third-party verification.

Social bonds finance job creation, socioeconomic advancement, empowerment, affordable housing, access to education, and/or vocational training.

Sustainable bonds or loans are bond issues in which the issuer commits to use the proceeds to finance green and social projects. The issuer commits to allocating proceeds to environmental and social projects according to a predefined set of eligibility criteria.

Given the wide variety of green bonds and the absence of a centralized market, conferring with your financial advisor you may find the appropriate green bond for you.

The Climate Bonds Initiative has awarded over 235 organizations, financial institutions, and governments that have demonstrated leadership through financing climate-resilient and low-carbon projects across a wide range of industries and economic sectors over the last nine years. In 2023, some of the most interesting awards included:

California Community Choice Financial Authority for the Largest US Green Municipal Issuer of 2023 (tax-deductible).

New York City Housing Development Corporation for the Largest US Social Sustainability Municipal issuer of 2023.

Morningstar Sustainalytics for the Largest External Review Provider in the Number of Deals of 2023 and Largest Verifier of 2023.

IBRB World Bank for the Largest Sustainability Bond of 2023.

Republic of Italy for the Largest Green Bond in 2023.

Sixty-two percent of American adults own equity. If you believe that the earth is warming, get paid to help the poor planet by buying a Green Bond.

References

Bhattacharya A, Songwe V, Soubeyran E and Stern (2024) Rasing Ambition and Accelerating Delivery of Climate Finance. London: Grantham Research Institute on Climate Change and the Environment, London School of Economics and Political Science.

Shorrocks A, Davies J and Liuberas R (2021) Global wealth report 2021, Credit Suisse Research Institute.